Decoding SEBI’s New Mutual Fund Categorisation Norms - I : Major Takeaways

- Akshay Nayak

- Mar 6

- 5 min read

On 26th February 2026 Securities and Exchange Board of India (SEBI) issued a circular that carries multiple pervasive implications for the mutual fund industry. Needless to say, there is just as much for mutual fund investors to take away too. The circular mostly focuses on categorisation of mutual funds. It also impacts the way certain categories of mutual funds operate. There is a lot to unpack. And that is going to be the focus of today's post. I am going to highlight and decode the major takeaways the circular offers investors.

Discontinuation Of Solution Oriented Funds

Such funds are most popularly advertised for use in case of major financial goals. The most popular use cases for such funds arise in context of planning for retirement and higher education. They come with lock in periods. The way in which solution oriented schemes work has been laid out in the graphic below.

But they are essentially quite similar to hybrid mutual funds. So there is no practical need for solution oriented funds to be treated as a separate category. Accordingly the circular now prohibits fresh subscription into such funds. Existing funds under this category are mandated to be merged with hybrid funds that have a similar asset allocation and risk profile. The merger would be effective subject to regulatory approval.

Stringent Restrictions On Overlap

The circular has major implications for sectoral, thematic value and contra funds. Mutual fund houses are now allowed to offer value funds and contra funds in parallel. But a cap of 50% has been imposed on overlap between thematic, sectoral, value and contra funds. In other words funds would be merged if there is an overlap of more than 50% between the holdings of :

A. Two sectoral or thematic funds

[OR]

B. A value fund and a contra fund

This effectively ensures that such funds would have distinct investment strategies. It also reduces redundancy of funds.

This prohibits the possibility of schemes with significant overlap being missold under different names. At present this is especially prevalent in the case of sectoral and thematic funds. Existing schemes have been allowed a transition period of 3 years to comply with the requirements of the circular. The move comes as a huge blow to the Asset Management Companies (AMCs). They would no longer be able to go on a spree of launching such funds under the pretext of gathering Assets Under Management (AUM).

Change In Composition Of Arbitrage Funds

Arbitrage funds are now mandated to invest their debt component solely in one year government securities (G-Secs). The move comes soon after the increase in Securities Transaction Tax (STT) announced during the most recent budget. The impact of these two developments is likely to hit the expected return of arbitrage funds. This may make arbitrage funds seem less attractive.

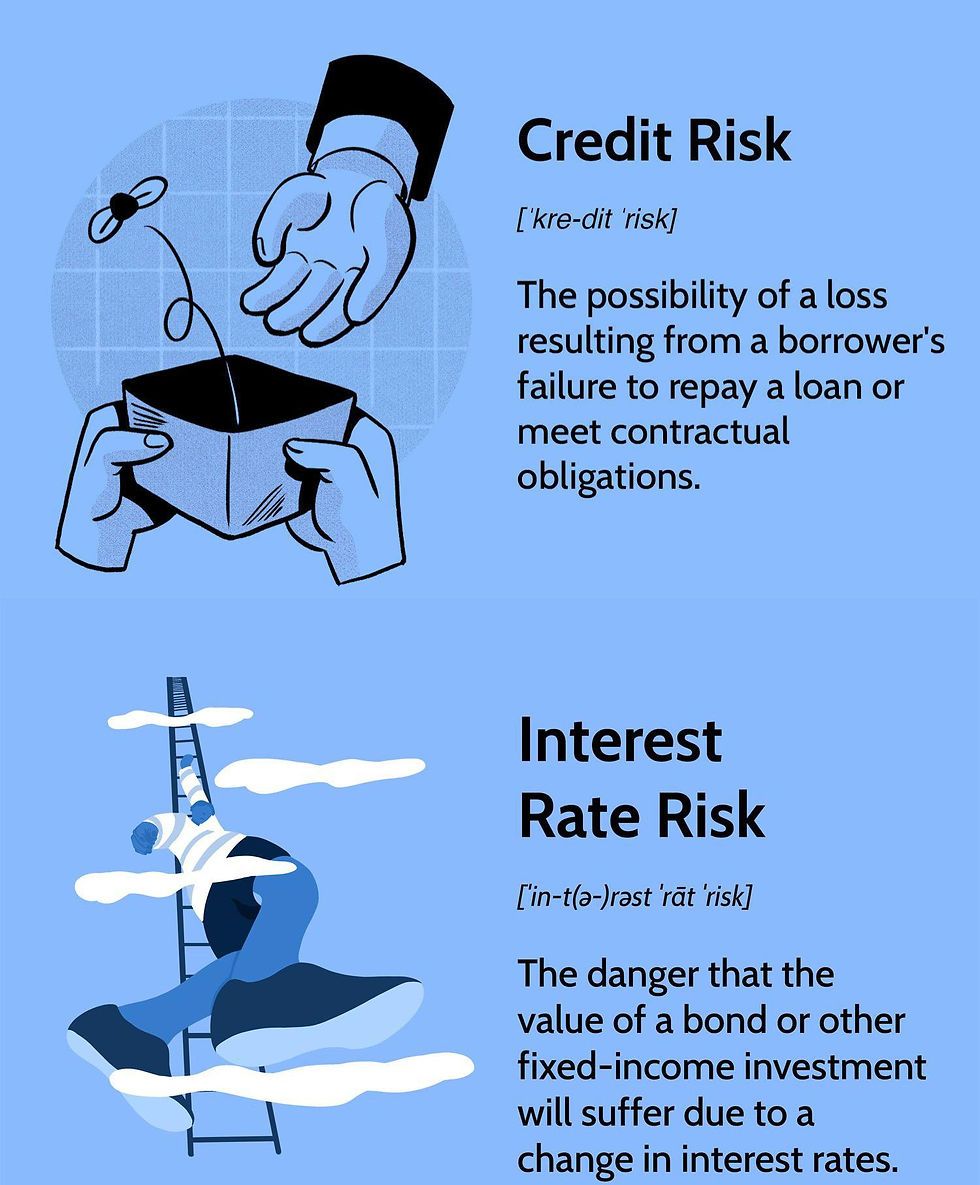

But I see things slightly differently. I feel that these changes make arbitrage funds a more viable option for our long term debt portfolios. The debt component of a long term portfolio is meant to provide stability and liquidity, not boost returns. Therefore the first principle to adhere to when constructing a long term debt portfolio is to avoid credit risk and interest rate risk. These are the primary sources of risk for a debt mutual fund.

Debt assets of arbitrage funds being invested solely in 1 year G-Secs means that both these risks are automatically reduced. But it must be remembered that arbitrage funds also have an equity component. So there is still a degree of risk associated with them. A fair degree of caution therefore remains a requirement if one decides to invest in them.

Introduction Of Sectoral Debt Funds

Sectoral debt funds are advertised to provide focused sectoral exposure to bonds while keeping credit risk low. Such funds are mandated to invest in bonds from 5 major sectors. These are financial services, real estate, energy, housing and infrastructure. Such funds must invest at least 80% of their assets in debt and debt related instruments from one of these sectors. The instruments held by these funds must have a credit rating of AA+ or higher.

This would help achieve the advertised objective of such funds. But 80% of the fund's assets being held in a single sector exposes it to concentration risk. Debt is meant to balance the high degree of risk that is inherent with equity in a long term portfolio. So it makes no sense to take on additional risk in our debt portfolios. Also, sectoral debt funds are only entering the market now. Their behaviour, risks and returns first need to be observed and studied over a considerable period of time. Only then can an informed decision be taken on their viability. So there is no need for anyone to be in a rush to invest in them.

Implications For Index Funds, ETFs, FoFs And Foreign Securities

Index funds and ETFs are now required to invest a minimum of 95% of their assets in securities of their respective benchmark indices. Domestic and overseas Fund of Funds (FoFs) are now required to invest a minimum of 95% of their assets in units of the underlying funds of the FoF. Foreign securities will no longer be treated as a separate asset class.

Introduction Of Lifecycle Funds

This is the most groundbreaking change introduced by the circular. Doing justice to the subject of lifecycle funds requires an article of its own. I will therefore touch upon the concept of lifecycle funds for now. The detailed analysis of lifecycle funds would be covered through a separate article in the future. Lifecycle funds are largely similar to target date funds.

These are open ended funds. They have defined maturities of 5 to 30 years. They also offer a preset glide path for asset allocation. This means the equity allocation in the fund would progressively reduce as the goal comes closer to falling due. Such funds have therefore been advertised as an ideal option for investors looking to follow a goal based approach to investing. We will understand how far this is true in the next article that will discuss lifecycle funds in detail.

Closing Thoughts

The changes discussed here are a select few among the many introduced by the circular. But they are the ones that impact investors the most. The circular definitely takes a number of steps in the right direction. It signals a fundamental reset of the Indian mutual fund ecosystem. It provides investors greater clarity and transparency on what they are picking for their portfolios. It reduces scope of products being duplicated and/or missold. Existing product offerings have been made truer to label than before. More such changes and reforms would definitely be welcome in the future.

Comments