Aspects Of Financial Decisions That Go Under The Radar

- Akshay Nayak

- Jun 12

- 4 min read

We all have our own approach to making financial decisions. Our methods are born out of our perceptions and experiences. So they are almost always likely not be well rounded and holistic. Most of our money decisions are likely to focus heavily on some aspects of each decision. Other aspects are likely to be ignored.

Naturally, most of our financial decisions would lack complete effectiveness. So today I am going to talk about the process we usually follow when making decisions regarding certain key areas of our finances. I will talk about the aspects that we usually focus on with regard to each decision. I will then show how the decision making process can be made more effective.

Buying A New Home

Our desire and decision to buy a new home is usually driven by emotions. Hence, we tend to overlook all other aspects surrounding the decision. We usually go through with the purchase as soon as we have enough money to make a downpayment. The rest would be financed by means of a home loan. But doing things this way ignores a lot of things.

Firstly, the demands that most careers place on us today have completely changed. Professional growth is likely to demand lot of travelling and relocating. So buying a house in one area early on in our careers would make little sense. This is because we are unlikely to use it for long enough to justify the costs incurred.

Moreover, EMIs today have become exorbitant. The kind of stress that EMIs can place on our finances is something that we rarely factor into our calculations. For example, paying an EMI of Rs 70,000 per month with a monthly income of Rs 1,00,000 would leave only Rs 30,000 available for other expenses and savings. Therefore, renting a house would be a much better option for the majority of our careers.

Rental payments are likely to be significantly lower compared to EMIs. Renting would also give us greater flexibility to switch between geographical areas should we need to relocate. The best time to consider buying a home would be around age 40 onwards. We would be in a much better place physically and financially to buy a house. Those who wish to fund a home through EMIs must ensure our EMI payments do not exceed 30% of our net monthly household income.

Buying A Car

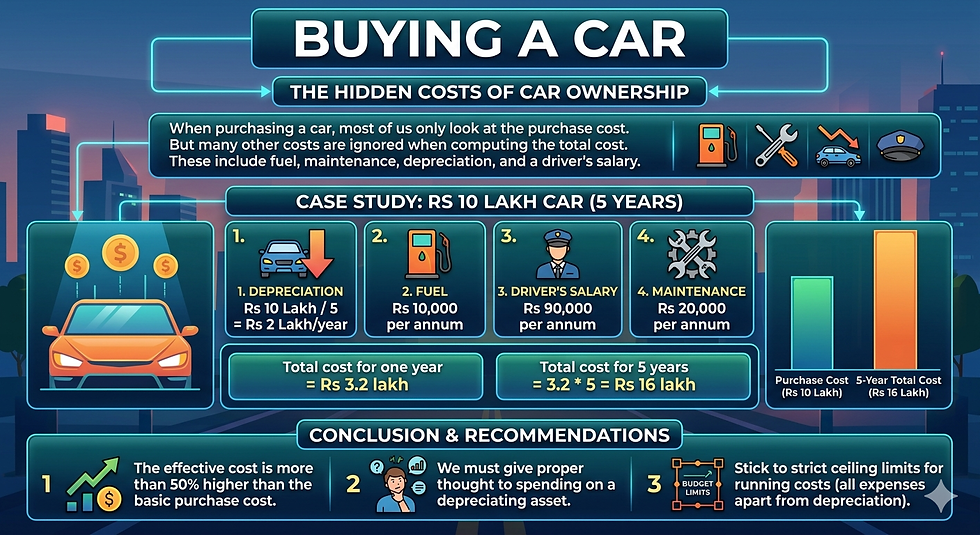

When purchasing a car, most of us only look at the purchase cost of the car. But there are a number of other costs that we ignore when computing the total cost of a car. These mainly include fuel costs, maintenance charges, depreciation, driver's salary (if any) and so on. Consider the following hypothetical estimated costs for an individual who purchases a car for Rs 10 lakh and intends to use it for 5 years. The residual value of the car at the end of its useful life is assumed to be zero. This would facilitate ease of calculation.

Depreciation = Rs 10 lakh/5 = 2 lakh/year

Fuel = Rs 10,000 per annum

Driver's salary = Rs 90,000 per annum

Maintenance = Rs 20,000 per annum

Total cost for one year = Rs 3.2 lakh

Total cost for 5 years = 3.2*5 = Rs 16 lakh

Clearly, the effective cost of the car is a more than 50% higher as compared to its basic purchase cost. We must therefore give proper thought as to whether or not we are willing to spend such amounts, especially on a depreciating asset. It would also help to stick to strict ceiling limits for each item of the running cost. This includes all expenses attributable to the car apart from depreciation.

Debt Management

We usually prioritise our debt payments from largest to smallest. And we do so based on the outstanding amount of each debt. Therefore, we end up focusing on our home loans first. We later move to other debts such as personal loans and credit card debt. But this ignores the interest cost associated with each of our debts. It is the interest cost which is actually responsible for our debts spiralling out of control.

Therefore our approach to debt management must focus on managing both the absolute amount and the associated interest costs. The Debt Snowball and Debt Avalanche methods are the best way to do this. The Snowball method focuses on the absolute amount of our debts. The way it works is laid out below :

List out all debts

Make minimum payments on everything

Pay extra on the smallest debt

Move on to the next-smallest debt

Repeat until all debts are paid off

The Avalanche method on the other hand focuses on the interest costs associated with each of our debts. The way in which it works is laid out below :

List out all outstanding debts

Pay extra on the debt with the highest interest rate

Move to the next-highest interest rate

Pay the minimum on everything else

Repeat until all debts are paid off

The Snowball method is therefore likely to be a good fit for those who find it psychologically challenging to pay off their debts. The Avalanche method is likely to be useful to those looking to optimise interest costs.

Final Thoughts

Clearly the less apparent aspects of each financial decision decide its effectiveness. Therefore these aspects deserve greater focus to ensure the most effective decision possible is made. This would promote financial stability and peace at all times.

Comments